By

Director of Climate Science & Impact

5 min read

The Science Based Targets initiative (SBTi) has published its long-awaited Corporate Net-Zero Standard V2, marking the most significant update to the framework since it was first introduced.

The revised standard strengthens instruction and accountability across a range of different business contexts, introduces new approaches to emissions reductions and raises the bar for how businesses demonstrate progress towards net-zero. And while the new standard offers greater flexibility in some areas, it also requires more robust governance, reporting and planning than ever before.

Our team has reviewed and analysed the finalised Corporate Net-Zero Standard V2, and we’ve listed the main changes that businesses need to understand below.

When does SBTi V2 come into effect?

Many organisations are working toward or waiting for SBTi validation on targets under the previous (V1.3) Standard, so the new V2 is not mandatory right away.

Until the end of 2027 businesses will be able to continue submitting new targets under the V1 Standard - though elements of the new Standard are also available under V1 under transitional arrangements.

From 1 January 2028, V2 will roll out in full, and businesses will have to certify against the new version from that date.

What is in the new SBTi V2?

Continuous accountability replaces one-off validation

One of the most significant changes is that SBTi validation is no longer treated as a one-time milestone. Instead, businesses are expected to demonstrate ongoing progress throughout the life of their targets.

The new framework introduces:

Revalidation cycles under a new SBTi Assurance Model.

Mandatory annual progress reporting.

Progress checks made by SBTi-recognised validation bodies.

Strong focus on taking accountability for ongoing emissions through climate contributions each year.

This means climate targets can no longer sit on the shelf after approval - the days of ‘set and forget’ are over, and in order to remain compliant, businesses will have to demonstrate that they are walking the walk on their emissions reduction goals.

Greater alignment to business capabilities

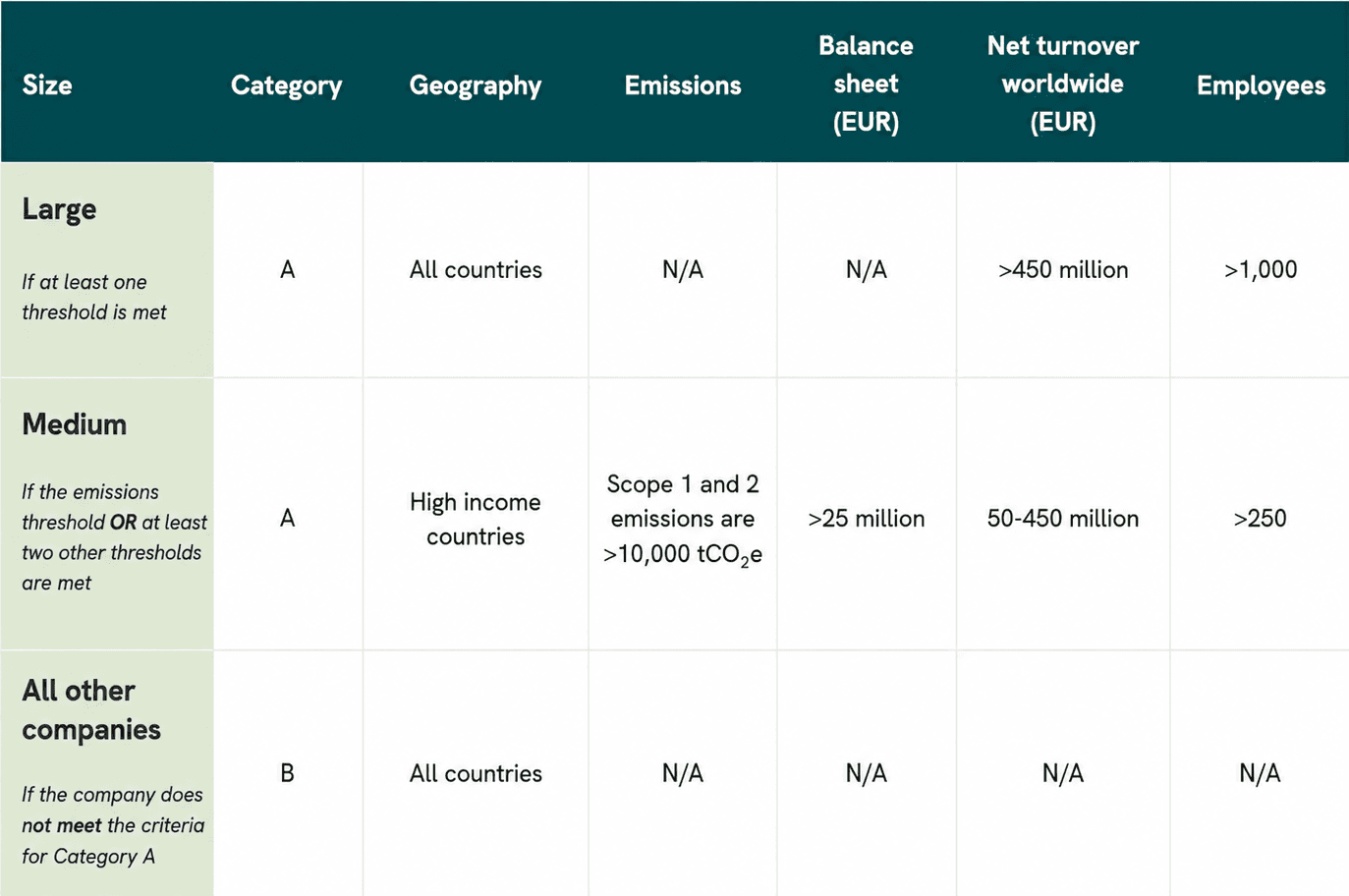

The introduction of Category A and Category B companies recognises that not every organisation has the same resources or level of influence.

Which category a business falls into depends on its size (defined using metrics like turnover or number of employees) and whether it is based in a high-income country (as defined by the World Bank).

Category B businesses benefit from proportionate flexibility around some requirements, including transition planning and implementation timelines, and obligations under the ‘Ongoing Emissions Responsibility’ framework. This will make science-based targets more accessible for many businesses.

All small companies are Category B, and as are medium companies from countries which are not high-income. Since the UK is a high-income country, medium and large businesses in the UK are all considered Category A.

Transition plans become a core part of climate strategy

The V2 Standard places much greater emphasis on how businesses intend to deliver their targets, not just what those targets are.

For all organisations, board-approved science-based targets and transition plans now form a central part of compliance. These plans are expected to set out delivery actions, financial implications, governance arrangements and fossil fuel phase-out strategies.

This board accountability is designed to support science-based targets with strong governance and enable businesses to make crucial decisions with the highest level of authority.

Scope 1 reductions become more realistic

One of the most practical improvements under the new Standard is the introduction of Asset Decarbonization Plans as an alternative approach for reducing Scope 1 emissions.

Rather than requiring linear reductions every year, businesses can now align emissions reductions with real asset replacement cycles and investment decisions. A given asset can therefore have its own decarbonisation plan - as long as it remains consistent with reaching net-zero by 2050. This is particularly beneficial for manufacturers, logistics companies and any organisation with long-lived infrastructure.

We think this is a more realistic approach, which allows companies to develop carbon budgets and asset-level decarbonisation roadmaps that better reflect operational realities, without being penalised.

Scope 2 renewable electricity rules become stricter

The new standard significantly tightens the credibility requirements around renewable electricity claims.

Businesses will need to pay much closer attention to where their renewable electricity comes from and how it is matched to consumption. Key changes include:

Restrictions on energy certificates for plants older than 15 years.

A move towards hourly matching for large electricity users, and a recognition programme for companies demonstrating leadership in this area.

A requirement to achieve 100% low-carbon electricity by 2050 at the latest OR reduce absolute scope 2 emissions to residual levels (<10% of baseline).

For organisations that have previously relied on standard renewable tariffs, procurement strategies will need to evolve considerably over the coming years.

Scope 3 reduction targets become more flexible

Supply chain emissions remain one of the biggest challenges for businesses, and the revised Standard changes how companies can approach them.

Businesses are expected to achieve net-zero across all Scope 3 emissions by 2050 at the latest, with a limited number of exclusions: any Scope 3 category that represents 5% or less of Scope 3 emissions; Category 3 (fuel- and energy-related activities) provided they are mitigated through consumption reductions under Scope 1 or 2 targets; and activities which lack a practical influence – for example when companies have no operational control over leased assets.

Another notable addition is the introduction of activity pools, allowing companies to support emissions reductions across groups of suppliers or regions without requiring direct supplier-by-supplier attribution. For businesses with complex or fragmented supply chains, this could make implementation considerably more practical.

Activity pools sit within a hierarchy of credible target delivery, where direct actions at the activity level are the highest priority, followed by activity pools, and finally sector-level reduction actions.

Governance moves into the boardroom

Perhaps the overarching theme of V2 is that climate action is no longer viewed solely as a sustainability function. The V2 on the whole is designed to drive real-world business transformations by embedding science-based targets into corporate decision-making at the highest level.

The V2 Standard places greater emphasis on board oversight, annual disclosures, documented dependencies and organisational accountability – all companies will now be required to have the board sign off on science-based targets and climate transition plans.

This is also likely to lead to greater success in achieving those targets – and greater business success in general. Companies that integrate climate planning into financial and strategic decision-making are likely to be much better positioned than those treating emissions reporting as a standalone exercise.

Brand new Ongoing Emissions Responsibility framework

One of the largest new additions in SBTi V2 is the introduction of the Ongoing Emissions Responsibility (OER) module, which combines ‘Beyond Value Chain Mitigation (BVCM)’ and neutralisation with carbon dioxide removals beyond the net-zero year into a single framework.

OER is designed to incentivise businesses to fund projects outside of their value chain (through carbon credits and philanthropy) on an ongoing basis each year, commensurate with their ongoing emissions. There are different rules for Category A and B companies, and different obligations after 2035.

The OER module is complex but in summary, it includes:

New recognition programme with an obligation to ‘comply or explain’.

Three tiers of recognition: “Engaged” and “Advanced” and “Leadership”.

Companies must meet a performance threshold against reduction targets to be eligible.

The coverage of ongoing emissions and method of contribution to projects varies by the recognition tier selected:

Engaged companies must cover at least 1% of total emissions (all scopes) with verified mitigation outcomes (e.g. carbon credits) OR establish a contribution budget based on the covered emissions (with a recommended $20 USD per tCO2e carbon price).

Advanced companies must cover 100% of Scope 1 and 2 emissions and additional Scope 3 emissions as necessary so that total coverage reaches >10% of all emissions. They must cover these emissions tonne-for-tonne with verified emissions outcomes OR establish a contribution budget based on a carbon price of $20 USD per tCO2e.

Leadership companies must cover 100% of total emissions (all scopes) and establish a contribution budget based on a carbon price of $80 USD per tCO2e. They must cover these emissions tonne-for-tonne with verified emissions outcomes and use the remaining budget to support further eligible climate contributions.

Recognition level | Coverage | Contribution budget approach | Application | Verified mitigation approach |

Engaged | 1% of total ongoing emissions | Covered emissions × carbon price per tonne (no mandated price) | OR | Verified mitigation outcomes equal in volume (tCO2e) to covered emissions |

Advanced | 10% of total ongoing emissions including 100% Scopes 1 and 2 | Covered emissions × minimum $20 USD carbon price per tonne | OR | Verified mitigation outcomes equal in volume (tCO2e) to covered emissions |

Leadership | Category A: 100% of total ongoing emissions Category B: 10% of total ongoing emissions (including 100% of Scopes 1 and 2) | Covered emissions × minimum $80 USD carbon price per tonne | AND | Verified mitigation outcomes equal in volume (tCO2e) to covered emissions |

From 2035, Category A companies must take responsibility for 1% of their ongoing emissions (all scopes) with carbon removals, including a minimum of 10% carbon removal with durable storage. Emissions coverage for mandatory OER increases linearly to 100% by the net-zero year.

For neutralisation at the net-zero year, companies must:

Neutralise 100% of residual emissions across all scopes.

Use a portfolio of carbon removal which covers all residual long-lived greenhouse gases with long-lived carbon removals.

Cover the remainder with further removals which can include short-lived (nature-based) removals.

Recommended (but not mandated) to ensure and disclose that removal credits are Correspondingly Adjusted wherever possible.

The SBTi also provides instruction on what kinds of projects businesses can fund under OER - which is similar to the eligible activities under the previous BVCM guidance, though further clarity about eligible activities has been provided.

What does SBTi V2 mean for your business?

Whilst sustainability practitioners in every business pore over the new SBTi Corporate Net-Zero Standard to understand its many new rules and implications, the overall direction of this draft is clear.

With the new version, businesses are expected to sharpen up: loopholes from the old version have been closed, and stronger requirements are in place to ensure that businesses are delivering on the climate action plans they are setting. There are also new flexibility mechanisms in place to make emissions reductions more realistic, and a whole new incentive scheme to help oblige businesses to fund climate action projects outside the value chain.

The new Standard changes things depending on where you are in your climate journey. Here's what's worth thinking about, based on where your business stands right now.

If you're not planning to set science-based targets, but you know supply chain pressure is coming

You might not be feeling urgency from regulators yet, but your customers probably are.

SBTi V2 raises the bar for what "good" looks like, and procurement teams are already using it as a benchmark. Getting your emissions measured now means you're not starting from scratch when the request comes in, and the businesses that move early tend to find the whole process far less painful than those who get pushed into it.

If you're actively considering setting science-based targets

SBTi V2 changes the structure of both near-term and long-term targets, and what qualified under V1 won't automatically qualify now.

Before you commit, it's worth understanding the gap between what you currently have, and what V2 actually requires – particularly around Scope 3 scope targets. Get that right, and a validated target becomes a genuine commercial asset rather than just a compliance exercise.

If you're pursuing a recognised sustainability standard or certification

Several frameworks update their alignment criteria in step with SBTi revisions, so it's worth checking whether the standard you're working towards has moved.

What's changed most under V2 is the emphasis on transparency and methodology. Your targets need to be publicly defensible, not just internally documented, and the evidence base behind them needs to be solid.

If you're aiming for real climate leadership

SBTi V2 sets a new standard for climate leadership, and leadership now means demonstrating continual alignment with the most current version of the Standard, and progress against your reduction goals – not just having a target. You’ll want to participate fully in the voluntary Ongoing Emissions Responsibility scheme too, to demonstrate that you are taking accountability for the emissions you are still producing on your pathway to net-zero.

Nature and biodiversity are also increasingly central, with V2 signalling a clear direction of travel that integrates ecosystem impact more explicitly into corporate commitments. The gap between businesses that look like they're leading and those that genuinely are is getting easier to spot.

If you’re not sure which category you fall into, or what V2 means for your company?

Talk to our team. We work with businesses at every stage of this and can help you figure out where you stand and what to do next.

Sam Jackson, Director of Climate Science and Impact at Ecologi